What is GAAP? Accounting basics for startups and small businesses

TL;DR

- GAAP ensures financial statements are consistent, comparable, and trustworthy to investors, lenders, and regulators. The standards are set by FASB in the U.S. and IFRS internationally.

- Core principles of GAAP include revenue recognition, accrual accounting, and consistent reporting methods that make results meaningful across periods and companies.

- Most small businesses, freelancers, and independent contractors don’t need to follow GAAP in the early days. However, GAAP principles should be followed when raising venture capital, securing large loans, or preparing for a sale.

- Non-GAAP reporting works for internal planning and projections, but carries less credibility with external stakeholders. Neither approach is inherently wrong.

- Start with a bookkeeper and centralized, reconciled data. Add accounting expertise as reporting gets more complex and your financials face scrutiny from external parties.

For fledgling businesses, accounting usually means little more than paying bills and tracking revenue and expenses. But sooner or later, someone will mention generally accepted accounting principles (GAAP) and you might think, “What is GAAP in accounting — and how does it affect me?” GAAP is a trusted, standardized way of preparing financial statements. By following GAAP, anyone evaluating your business can easily understand your statements and reliably compare them to other companies’ financials.

Some companies need to follow these rules early on. For others, GAAP is something to keep in mind for the future. Understanding what GAAP is, when it matters, and how to prepare for it can keep you from being caught off guard later. Read on for a GAAP definition explained in simple terms.

What are the GAAP principles?

When you first start keeping books, you might think of accounting as simply recording what money comes into your business and what goes out. But, over time, there are third parties who may need more information than that — people like investors, auditors, and lenders. That’s where GAAP comes in.

Generally accepted accounting principles (GAAP) are set by the Financial Accounting Standards Board in the U.S. The purpose is to make financial reporting consistent, comparable, and reliable.

Core GAAP accounting principles include:

- Revenue recognition: how and when income is reported

- Accrual vs. cash accounting: whether you record money when it actually changes hands (cash) or when a bill or invoice is created (accrual)

- Consistency and comparability: using methods that allow fair comparisons over time

These standards prevent what’s sometimes called “creative accounting” — methods that make a business look healthier than it really is. Without GAAP, two companies could report completely different versions of their financial health, even if their operations are similar. For example, one business might record revenue the moment a contract is signed while the other waits until cash hits the bank, making their results impossible to compare.

Investors and lenders depend on GAAP to make apples-to-apples comparisons and to avoid being misled. For founders, that means adopting GAAP isn’t only about compliance, it’s also about building trust and credibility, which can open doors to funding opportunities or partnerships later.

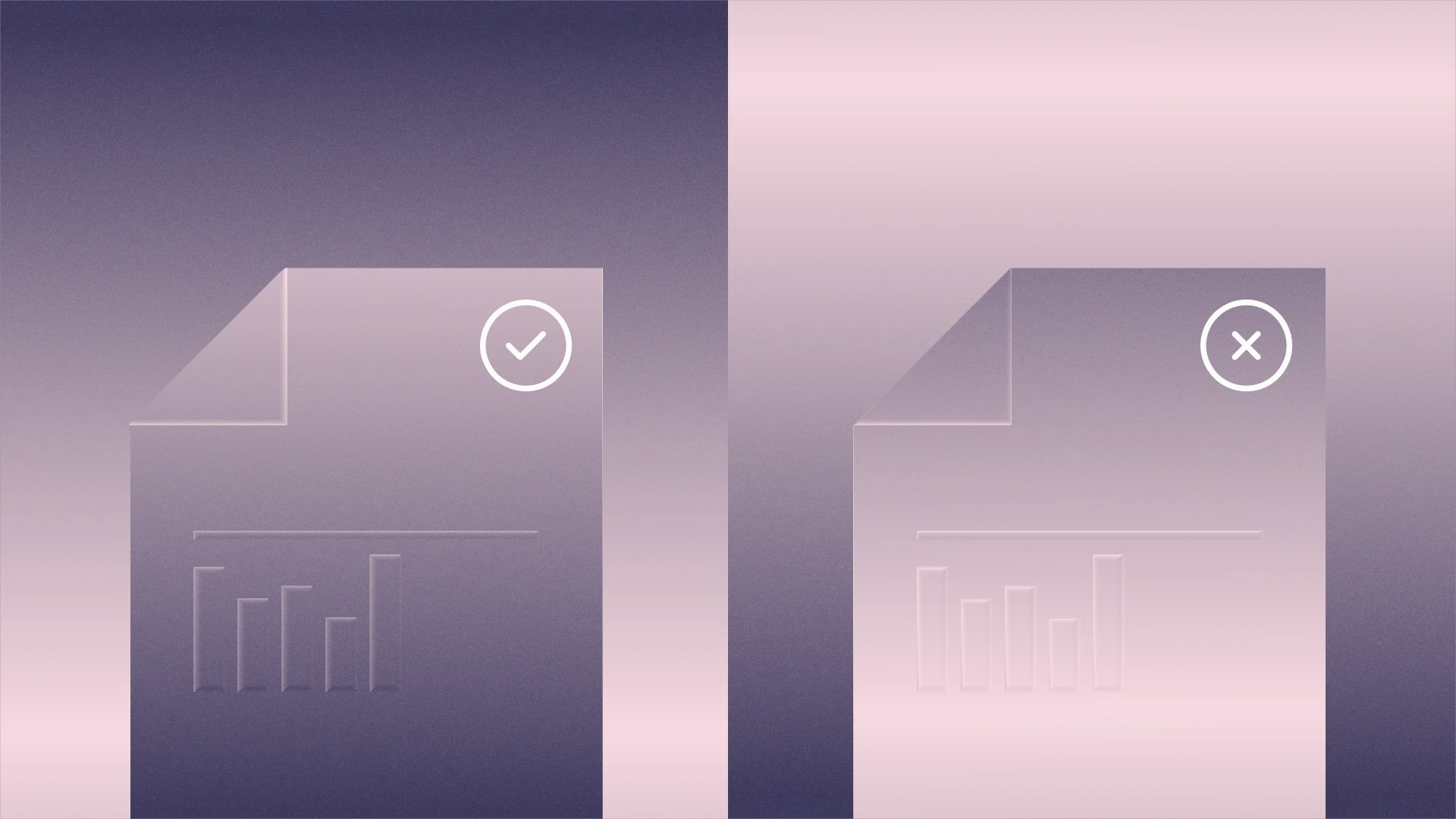

GAAP vs. non-GAAP: What’s the difference?

Financial results can look very different depending on how you present them. A set of financials that looks one way under GAAP might look different if you leave out one-time expenses or unusual costs. That’s why companies often talk about GAAP and non-GAAP results.

Here’s the contrast between GAAP and non-GAAP approaches in plain English.

GAAP | Non-GAAP |

Standardized; required for audited statements | Flexible; company-defined |

Ensures comparability and transparency | Can exclude unusual or one-time items |

Trusted by banks, investors, regulators | Useful for internal planning, storytelling, and projections |

More complex and sometimes costly | Simpler, but less credible externally |

To see the difference in practice, imagine you run a startup that invested in a costly piece of equipment. Under GAAP, that expense has to be recorded, which may make your year look less profitable. Internally, though, you might create a non-GAAP version of your financials that excludes that one-time cost to give you a clearer view of the company’s recurring profitability.

Neither method is “wrong.” GAAP offers credibility and comparability for external stakeholders, and non-GAAP accounting can give founders a clearer look at day-to-day performance. The key is understanding which to use, and when.

Maintaining a balance between the two is easier when your systems sync. Mercury’s accounting automations can help keep your internal numbers and GAAP reporting aligned by connecting directly to QuickBooks or Xero.

Note: Outside of the U.S., many businesses use International Financial Reporting Standards (IFRS). The two systems overlap, but aren’t identical. That’s why investors sometimes ask about the difference between GAAP and IFRS, when companies operate internationally.

Does my business need to follow GAAP?

Not every small business has the same accounting needs. What works for a freelancer won’t work for a startup that’s getting ready for investors. To determine whether or not GAAP applies to you, consider where you are in your business journey and where you want to go next.

Follow GAAP if:

- You’re planning a venture capital raise or applying for a large institutional loan.

- Your business needs audited financial statements.

- You’re operating as a public company or in a tightly regulated industry.

Consider GAAP if:

- Your company is on track for rapid growth.

- You expect to sell the business or merge with another in the future.

- You want to avoid the hassle of redoing years of financial reports later.

Skip GAAP if:

- You’re freelancing or working as an independent contractor.

- You manage a very small team.

- Your records are mainly for taxes and basic compliance.

Think of GAAP accounting like road infrastructure. A two-lane highway might work for a city where traffic is light, but, if you know growth is coming, you’ll want to build in the extra capacity up front. Pairing your banking with a business card that gives you spend controls, clean transaction data, and easy accounting integrations makes it simpler to keep reports accurate and investor-ready.

What GAAP means for your systems

Even if you don’t need GAAP yet, the way you set up your financial systems today can make compliance easier later. Most accounting software — like QuickBooks, NetSuite, and Xero, for example — can generate GAAP-compliant statements. But those reports are only as good as the data you feed them. If your transactions are spread across multiple accounts, cards, and spreadsheets, pulling everything together takes time and increases the chance of errors.

One of the biggest challenges here is reconciliation — making sure your bank, card, and accounting records all match. Small mistakes can add up quickly, leading to unreliable reports. Since GAAP depends on accuracy, gaps in your data can create serious problems. Automations help close that gap by syncing transactions directly into your accounting system. This not only saves time but also reduces human error, leaving you with financial statements that are cleaner, easier to audit, and more likely to meet GAAP standards.

Centralization helps. Mercury’s accounting automations provide easy access to all your accounting data, and the unified financial workflows dashboard pulls your banking, invoices, and payroll into a single dashboard. Together, these products streamline reconciliation and ensure your accounting software is working with accurate, up-to-date data.

What GAAP means for your team

You don’t need a CFO on day one. Many founders start with a bookkeeper to get expenses and receipts in order. As things become more complex, an accountant can step in to prepare GAAP-compliant statements and help you stay on track for growth. GAAP is really about discipline — and that’s easier when you’ve got the right people in your corner. Even occasional guidance from a professional can save you from costly mistakes and give you confidence that your numbers are ready for investors, lenders, or auditors.

The bottom line

Most small businesses don’t need GAAP principles right away. Freelancers and bootstrapped founders can usually stick with solid bookkeeping and tax compliance. If you’re preparing for funding, growth, or a sale, though, GAAP will be expected — and being able to clearly answer the question, “What are the GAAP principles?” shows you’re ready for that next step.

Staying organized makes the shift easier. By connecting your banking, credit card spend, and accounting software all in one place, your records stay accurate, comparable, and investor-friendly.

Ready to simplify your accounting? Try Mercury’s accounting automations to manage bills, expenses, and transactions all in one place — and build a system that will grow with you.

What does GAAP stand for?

GAAP stands for Generally Accepted Accounting Principles. It is a standardized set of accounting rules set by the Financial Accounting Standards Board (FASB) to make financial reporting consistent, comparable, and reliable.

What are the core GAAP accounting principles?

The core principles of GAAP cover revenue recognition (how and when income is reported), accrual vs. cash accounting (whether you record money when it changes hands or when a bill is created), and consistency (using methods that allow accurate comparisons over time).

Is GAAP required for small businesses?

GAAP is not always required for small businesses. Freelancers and bootstrapped founders can usually stick with solid bookkeeping and tax compliance. GAAP becomes important when you're raising venture capital or applying for a large loan. It’s required when you need audited financial statements or operate as a public company.

What's the difference between GAAP and non-GAAP accounting?

GAAP has specific requirements and is required for audited financial statements. Non-GAAP is flexible and company-defined. Non-GAAP is useful for internal planning but has less credibility externally.

What's the difference between GAAP and IFRS?

GAAP is the U.S. standard. IFRS (International Financial Reporting Standards) is used outside the U.S. The two methods overlap but aren't identical, which matters when companies operate internationally.

Why is GAAP important for startups seeking funding?

GAAP builds credibility with investors and lenders by ensuring consistent reporting and preventing creative accounting. Adopting GAAP signals that you're ready for funding, growth, or a sale.

How can I prepare my business for GAAP compliance?

To prepare for GAAP compliance, set up accounting software (QuickBooks, NetSuite, or Xero) that can generate GAAP-compliant statements. You should also make sure your transactions are centralized and accurately synced to your accounting software.

When should I hire accounting help for GAAP?

Many founders start with a bookkeeper to organize expenses and receipts. Later, they bring in an accountant as complexity grows and GAAP-compliant financial statements become necessary.

Related reads

What is spend visibility and why does it matter?

How to build a spend management strategy from scratch

Spend management best practices every CFO should know