The future of banking*

Co-founder and CEO of Mercury.

I started my first company in 2006. Legacy banking in 2026 still works the way it did then. You deposited money into a vault, withdrew it to pay your bills, and if you needed anything more sophisticated like an MCP, you’d get confused looks.

Creating a radically different way for founders to do banking is the reason Jason, Max, and I started Mercury in 2017. Money is at the core of most business decisions, and yet legacy banks, the things that hold your money, don't help you make those decisions. Nine years in, and we’re not done.

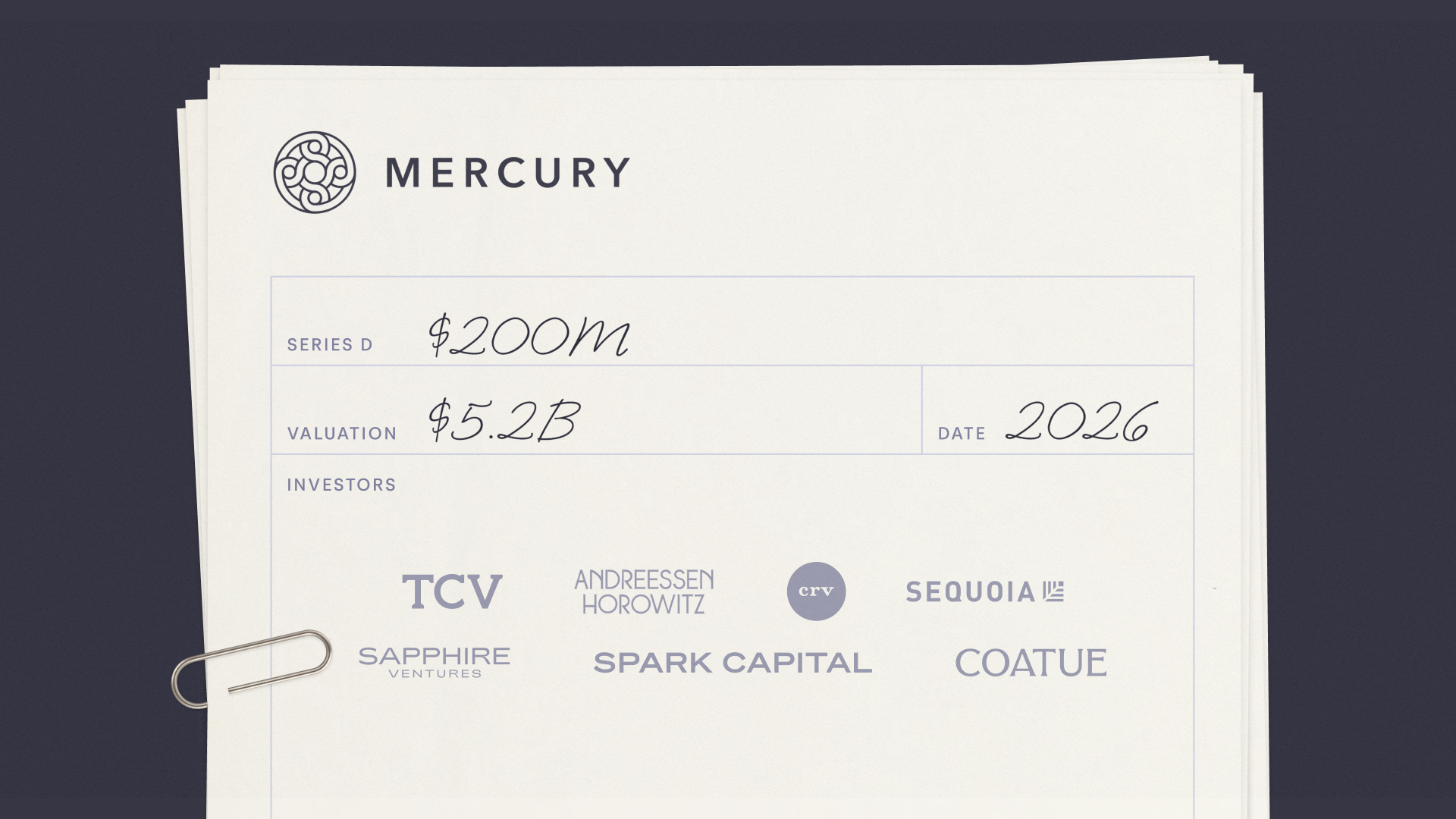

Today, we’re announcing a $200 million Series D at a $5.2B valuation. We’re excited to bring on TCV as our lead investor in the round, as well as returning investors Andreessen Horowitz, Coatue, CRV, Sapphire Ventures, Sequoia Capital, and Spark Capital.

This fundraise comes at an inflection point for entrepreneurs and the world. AI is collapsing the friction between an idea and a company faster than anything I have seen in my career. Q1 2026 saw an 18% increase from Q1 2025 in new U.S. business applications, according to the U.S. Census Bureau. Mercury saw a 2.5x increase in applications over the same period. Some of that is Mercury’s growing market share, but it also indicates a real shift in how many people are now starting to build new things. We are going to see more founders in the next five years than in the last 20. Mercury was created for this moment. We intend to meet it.

We raised because the opportunity in front of us is bigger than anything we’ve seen. The new generation of founders using AI tools deserve banking that helps them actually understand and run their businesses.

What Mercury looks like today

More than 300,000 customers choose Mercury, including one in three U.S. startups and a rapidly growing share of AI companies. Some of the most consequential tech companies being built today are Mercury customers: Supabase, ElevenLabs, Lovable, Linear, Phantom, and Tempo.

Mercury was built for tech startups, but we’ve grown well beyond that. Today, more than 73% of new customers come from outside the AI and tech startup category. We serve ecommerce companies like Bogey Bros and Cocolab, and professional services companies including Ways & Means and neuemotion. Individuals such as podcaster Dwarkesh Patel use Mercury for both business and personal finances.

4 years

Consecutive GAAP net income and EBITDA profitability

$650M

Annualized revenue, as of Q3 2025

73%

Of new customers come from outside the AI and tech startup category

300K+

Customers trust Mercury

What we built in the last year

That foundation let us build differently this year. Your account sees everything that happens with your money. We shipped products that actually use that knowledge, making Mercury a part of how your business runs. We introduced:

- Mercury Insights: Our first in-product AI tool, giving you an interactive, real-time view of your company’s financial health without exporting anything to a spreadsheet.

- MCP and CLI: AI developer tools that provide secure access to your Mercury account and the ability to take actions directly in the terminal.

- AI-native payroll: With our acquisition of Central we’ll bring payroll directly to your Mercury account.

- Mercury Personal: The same radically different banking experience, now available for qualifying U.S. applicants for their personal finances.

Where we’re headed with AI

Later this year, we’ll introduce Mercury Command, a new way to complete financial work end-to-end with AI.

Managing money today still means jumping between tabs, exporting data into spreadsheets, and reconciling competing information across tools. Command changes that. Instead of searching for what you need, you simply tell Mercury what you need and it happens: check your cash position, change your auto-transfer rules, categorize transactions, send an invoice — all in natural language and without leaving your account. Because Command is built directly into Mercury, every answer is grounded in real account data, and every action is reviewed and approved by the customer.

A milestone in becoming a bank

This raise comes on the heels of something we’ve been working toward for years. In April, Mercury received conditional approval from the OCC to establish Mercury Bank, N.A. and put us on a direct path to becoming a fully regulated national bank.

I’ve always believed Mercury should control more of the infrastructure that our customers depend on. A bank charter makes that possible in ways that matter: Zelle, an expanded suite of lending products, and deeper payment infrastructure we build and own ourselves.

We still have work to do before Mercury Bank opens its doors, including additional approvals from the FDIC and Federal Reserve and final approval from the OCC. But conditional approval is the OCC telling us that what we’re building is worthy of direct federal regulation. That means a lot.

None of this happens without our customers, team, and the investors who believe in what we’re building. The bank of the future knows your business. No legacy bank was built that way. We’re building it.

*Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC. The IO Card is issued by Patriot Bank, N.A., Member FDIC, pursuant to a license from Mastercard International Incorporated.

About the author

Co-founder and CEO of Mercury.

Share article

Related reads

Mercury applies for OCC national bank charter to become the bank for builders

Mercury enters payroll