If you’re watching the headlines, it’s tempting to assume business credit card fraud is only a big-company problem. In reality, it’s also a growing threat for startups, small businesses, and even everyday consumers. Scammers increasingly target smaller companies because these businesses often lack the fraud prevention resources that larger enterprises can afford. The fallout from even one instance of small business credit card fraud can ripple through your cash flow, operations, and your relationships with partners and customers.

Whether you’re a founder or a finance lead, fraud is a risk that should be on your radar, especially in the early days when your company’s budget is tight and revenue is uneven. A recent Experian report shows that fraud incidents impacting small businesses have risen by 70% over the past five years.

The good news? You don’t need a dedicated risk department to stay safe. By learning about credit card fraud prevention for businesses — including the most common types of fraud and practical safeguards — you can dramatically reduce your company’s exposure. And, if fraud does happen, having a clear fraud response plan at the ready will help your business recover quickly.

Four common types of business credit card fraud

Fraud can take many forms, but most incidents fall into a handful of categories that every business owner should recognize.

Lost or stolen card fraud

Lost or stolen credit card fraud is common in growing businesses where multiple employees carry physical cards for travel or day-to-day purchases. A missing card might not raise alarms right away, but, by the time it’s noticed, fraudsters might already have gained access and charges could be stacking up.

Card-not-present (CNP) fraud

Fraudsters can easily make online purchases without having access to a physical card. A stolen credit card number, often bought on the dark web after data breaches, is enough for online purchases. For startups that rely heavily on cloud-based tools and digital advertising (in other words: most startups), this is one of the most common and costly fraud risks.

Account takeover fraud

Phishing schemes and other social engineering techniques can give criminals access to your accounts. Once they’re in, they can change settings, request new cards, or authorize fraudulent transactions that look legitimate. Because the activity originates from your account, it often takes longer to catch, which means it can be more damaging.

Friendly fraud and chargebacks

Fraud doesn’t always start maliciously. A client might claim that they never received a product, or fail to recognize a charge on their credit card statement. These disputes can drain revenue, lead to fees, and force your team to spend time on resolution instead of growth.

Once you learn to recognize these patterns of business credit card fraud, you’ll be able to spot red flags faster and put guardrails in place before the issue escalates.

How credit card fraud affects businesses

Fraud isn’t just an inconvenience, it also slows growth and damages trust. Here’s how credit card fraud affects businesses.

Direct financial losses

Even if your credit card issuer reimburses you, fraudulent charges can tie up funds you need for payroll, inventory, or operations. For bootstrapped founders, waiting weeks for a resolution can be painful. In some cases, you may still be responsible for fees or chargeback costs.

Disruption of cash flow

Responding to fraud often means you have to cancel cards or freeze accounts. This could leave you scrambling to cover expenses while you wait for replacements. That might mean delaying payroll, running low on inventory, or missing a time-sensitive opportunity.

Damage to vendor, employee, and customer trust

Vendors and employees still expect payment, regardless of your financial situation. If you don’t meet your financial commitments, that can seriously strain relationships. And, if you aren’t able to ship orders to customers in a timely manner, you may start receiving expensive chargebacks. Both of these scenarios can also take a toll on your company’s bottom line — and your reputation.

Operational drag

Investigating fraud, disputing transactions, and tightening controls takes valuable time away from building your company. The losses don’t stop there, either. Every dollar lost to fraud can multiply once you add in the cost of admin hours, legal fees, and lost productivity.

Business credit card fraud prevention strategies

Business credit card fraud protection is most effective when it’s layered. No single tactic is enough, but having multiple strategies in place can dramatically boost your security.

Want to learn how to prevent credit card fraud for businesses? Here are four simple strategies.

Use modern card control features

Set spending limits, restrict spending categories, or lock cards to specific vendors. A $500 daily cap on a marketing card, for example, limits exposure if credentials are stolen.

Issue virtual cards

Instead of reusing one physical card across vendors, generate unique virtual cards for subscriptions, contractors, or one-time purchases. If a vendor or card is ever compromised, you can cancel it without disrupting the rest of your operations.

Enable real-time monitoring

Fraud often succeeds because it goes unnoticed. Setting up instant alerts and monitoring dashboards allows you to spot suspicious activity early and act quickly.

Educate your team

Many fraud attempts start with phishing. Train employees to use secure login practices, question unusual requests, and recognize and report other red flags.

Reconcile accounts regularly

Reviewing transactions weekly or monthly will help you catch small anomalies before they escalate. Plus, this practice will keep your books accurate.

By mixing proactive monitoring with strategic credit card features, you can create a level of security that rivals much larger companies.

What to do if fraud happens

Even once you invest in small business credit card fraud protection, it’s important not to get complacent. Keep an eye out for red flags and act fast if you notice something suspicious, to limit impact. Here’s what to do.

Step 1: Freeze or cancel the card right away

If you see an unexpected or suspicious transaction, lock or deactivate the associated card to prevent any additional charges.

Step 2: Contact your credit card provider

Report fraudulent transactions right away. Most providers have clear processes for disputing charges and protecting your funds and are ready to deploy them as soon as you say the word.

Step 3: File disputes and keep documentation

Save receipts, invoices, and communications related to the fraudulent charges. Documentation strengthens your case and speeds resolution.

Step 4: Update security practices to prevent repeat attempts

A fraud incident doesn’t have to derail your business. Act proactively as soon as you suspect an issue. Figure out how the fraud happened and patch the gaps with new prevention strategies. This might mean stricter card controls, stronger password policies, or additional employee training.

Putting strong business credit card fraud prevention strategies in place will help you to mitigate the impact, recover your funds, and build your defenses against future attacks.

Common mistakes to avoid

The biggest mistake is assuming fraud won’t happen to your business. Waiting until after an incident to put protections in place means you’re always reacting to fraud instead of preventing it. A reactive approach increases risk, takes more time, and is typically a lot more expensive.

Other common mistakes include:

- Using the same card across multiple vendors

- Putting off employee cybersecurity training

- Ignoring small discrepancies during reconciliations

Closing these gaps makes it easier to protect your finances, so you can stay focused on growing your business. .

Fraud is inevitable — but manageable

For startups and small businesses, protecting against credit card fraud can feel overwhelming, but it doesn’t have to be hard. Understanding the risks, putting preventative measures in place, and knowing how to respond if it happens are the pillars of business credit card fraud protection.

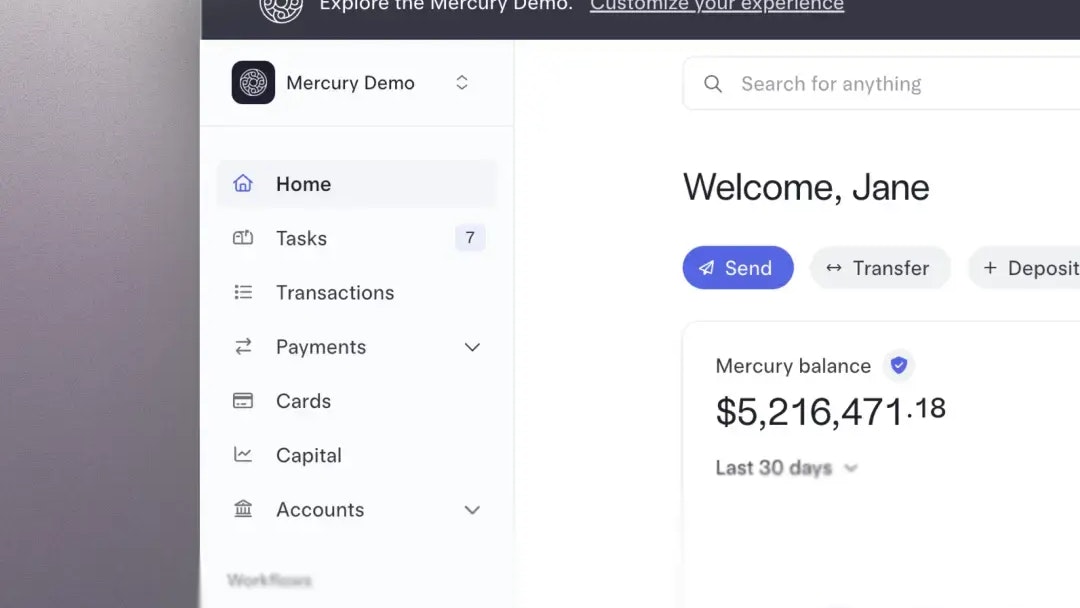

With tools like virtual cards, real-time monitoring, and built-in security controls, you can protect your company, without adding complexity. Mercury IO combines these safeguards with flexible expense management and fraud protection designed for ambitious businesses, giving you the confidence that your financial foundation is as secure as possible.

Ready to strengthen your defenses? Explore Mercury's IO credit card and see how a smarter, safer business credit card can preserve your company’s cash flow, operations, and reputation.